If you’ve spent any time researching the average cost of dental implants, you’ve likely hit a wall of frustration. You’ve paid into your dental insurance for twenty, perhaps thirty years, yet the moment you need a life-changing procedure, your provider suddenly treats it like an elective luxury.

It is the industry's most frustrating paradox. You are quoted $40,000 for a full-mouth restoration, and your insurance company graciously offers to contribute $1,500.

Most patients in their 50s and 60s enter my office asking about the bottom-line price. But as a patient advocate, I know the real battle isn't just the sticker price—it’s navigating the "insurance traps" that leave patients footing 90% of the bill. In this guide, we are pulling back the curtain on the insurance shell game, explaining exactly when your policy will show up for you, and when you are truly on your own.

The first thing you must understand is that dental insurance is not "insurance" in the traditional sense. Medical insurance is designed to protect you against catastrophic loss. Dental insurance, however, is a tax-advantaged maintenance coupon.

Since the 1970s, the "Annual Maximum Benefit" for most PPO plans has remained stagnant at roughly $1,500 to $2,500. While the average cost of dental implants has tracked with modern medical inflation and high-end technology, your coverage has been frozen in time.

This is the single most common reason for claim denials. Many premium plans include a clause stating that if the tooth was lost before you joined that specific insurance plan, they will not pay one cent toward its replacement. This is essentially a "pre-existing condition" exclusion that is still perfectly legal in the dental insurance world.

Pro Tip: Before you commit to a surgery date, ask your coordinator to perform a "Pre-Determination of Benefits." This forces the insurance company to state in writing what they will pay before the first incision is made.

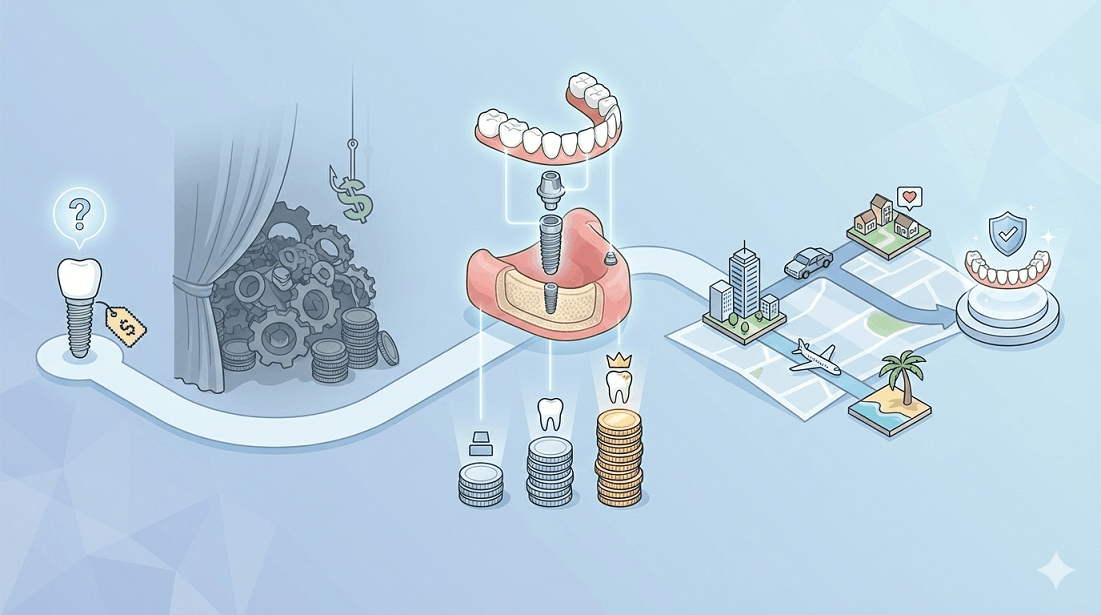

It isn't all bad news. While insurance rarely covers the entire procedure, savvy patients can maximize their "coupons" by understanding how codes are billed. A dental implant is typically billed in two distinct phases: the Surgical Phase and the Restorative Phase.

This is where insurance is most likely to fail you. Most providers view the titanium post (the implant itself) and the bone grafting required to support it as "elective." Even if they do cover it, it often falls under "Major Services," which may have a 12-month waiting period.

This is your best chance for coverage. Insurance companies are much more comfortable paying for the abutment and the crown. Because a crown is a standard dental restorative procedure, many plans will cover 50% of this portion, up to your annual maximum.

Pro Tip: If your treatment spans across two calendar years (e.g., surgery in December, crown in March), you can sometimes "double-dip" by using your 2025 maximum for the surgery and your 2026 maximum for the prosthetic tooth.

While dental insurance is stingy, your Medical Insurance can sometimes be a secret weapon. This is where "insider-savvy" advocacy makes a difference.

According to data tracked by the American Association of Oral and Maxillofacial Surgeons (AAOMS), dental implants are often medically necessary for patients with specific systemic conditions. If your tooth loss is a direct result of the following, your medical insurance (Health insurance) may cover a significant portion:

To unlock this, your surgeon must provide a "Letter of Medical Necessity." This letter must argue that the implant is not for "looks," but to prevent further bone degradation or to restore basic digestive function.

Because insurance covers so little, the average cost of dental implants is largely dictated by the quality of the clinic and the materials used. In 2026, you will see three distinct "tiers" of pricing. Insurance will treat all three the same, meaning the higher the tier you choose, the more you will pay out of pocket.

If your insurance is only offering you $2,000 toward a $40,000 case, you have to be smart about how you spend the remaining $38,000. Smart patients don't look for "cheap" surgery; they look for Domestic Arbitrage.

In major hubs like NYC or Los Angeles, clinic overhead is astronomical. Moving your search just a few states away to high-volume centers in states like Texas, Arizona, or Utah can often save you 30-40% on the total bill. This saving often dwarfs any benefit your insurance would have provided.

Avoid clinics that bill "a la carte." When a clinic offers Flat-Fee Pricing, they are absorbing the risk of the surgery. If you need an extra bone graft or a different type of abutment, you don't get hit with a surprise $2,500 bill that your insurance will inevitably deny.

Since insurance covers so little, the Health Savings Account (HSA) or Flexible Spending Account (FSA) is your best friend. These allow you to pay for your implants using pre-tax dollars, which effectively gives you a 20-30% discount depending on your tax bracket.

Pro Tip: If you have a high-deductible health plan, max out your HSA contributions the year before your surgery. It is the only "guaranteed" way to save money on the total cost without sacrificing the quality of the surgeon.

Choosing a dental implant provider based solely on the average cost of dental implants—or based on who your insurance provider "prefers"—is a dangerous gamble. In 2026, quality clinics are moving away from insurance dependency because it restricts the quality of care they can provide.

The informed patient wins by treating insurance as a "bonus" rather than a deciding factor. You win by prioritizing the surgeon's complication rate, the quality of the zirconia, and the transparency of the pricing.

Don’t guess with your health or your wallet.

Our Dental Implant Cost Evaluation compares local US pricing, state-to-state savings, and vetted international options — customized to your mouth and your goals.

Get your personalized report today.